GST rate hike from 7% to 9% over 2 years

The rate increase as follows:

- From 7% to 8% with effect from 1 January 2023 (first rate change)

- And the rate will increase from 8% to 9% with effect from 1 January 2024 (second rate change);

The gradual increment in GST rate is favourable decision for consumers, as it will give them additional time to adjust to the GST rate hike.

However, businesses will need to incur additional costs to amend their systems, contracts, for example twice given the gradual increment in the GST rate in 2023 and 2024.

The impact to GST registered businesses:

- Accounting and invoicing systems to incorporate new GST rates.

- Cash registers and receipting systems to incorporate new GST rate for point-of-sales billing.

For businesses that operate past midnight on 31 December 2023 up to 7am of 1 January 2024, can charge 8% on their sales made during this period if it is their normal accounting practice to treat the sales made after midnight as sales of the preceding day and their cash register and accounting system are programmed in this way.

GST registered businesses should update their price displays to reflect the new GST rate with effect from 1 January 2024 must inclusive of GST at 9%.

For businesses that are unable to switch price displays overnight, they may display two prices:

- One applicable before 1 January 2024 showing prices inclusive of GST at 8%; and

- One applicable from 1 January 2024 showing prices of GST at 9%

For businesses do not decide to increase prices, they do not need to revised price displays. However, will still need to account for GST based on the prevailing tax fraction (i.e., 9/109) for sales made on or after 1 January 2024.

Review contract

Generally, businesses should charge GST at 9% on supplies made on or after 1 January 2024 arising from existing contracts entered before 1 January 2024. Therefore, businesses should review their contracts with both suppliers and customers to ascertain the party responsible for bearing the cost resulting from the increase in GST rate unless the contract has explicitly specified that any tax change is excluded or has already been considered.

GST rate

GST rate chargeable on the supply will be the prevailing rate at the time of supply. For example, if businesses issue an invoice or receive payment for a supply before 1 January 2024, they should charge GST at 8%. Conversely, if businesses issue an invoice or received payment for supply on or after 1 January 2024, businesses should GST at 9%, unless businesses have elected to charge GST at 8% under transitional rules for rate change where allowable.

Transitional rules for rate change

Transitional rules apply to supplies which span the change of GST rate. Businesses may be required to adjust for GST rate chargeable on supplies and to account for GST at the new rate.

GST chargeable on most transactions should be based on time of supply rules as follows:

- Before 1 January 2023, 7%

- 1 January 2023 to 31 December 2023, 8%

- On and after 1 January 2024, 9%

If any of the following events happen on or after the date of the GST rate change, the supply is considered to span the change of GST rate:

- The issuance of invoice

- The receipt of payment (or the making of payment in respect of a reverse charge supply)

- The delivery of goods or performance of services (i.e. Basic Tax Point)

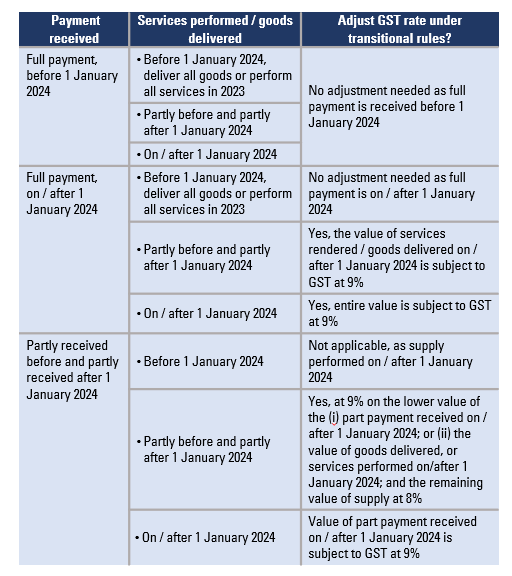

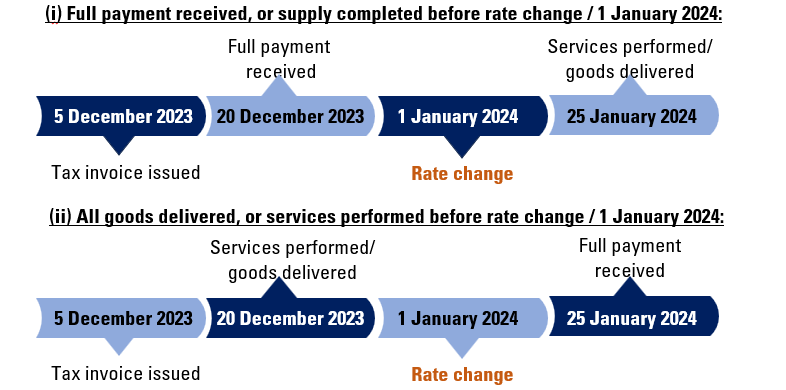

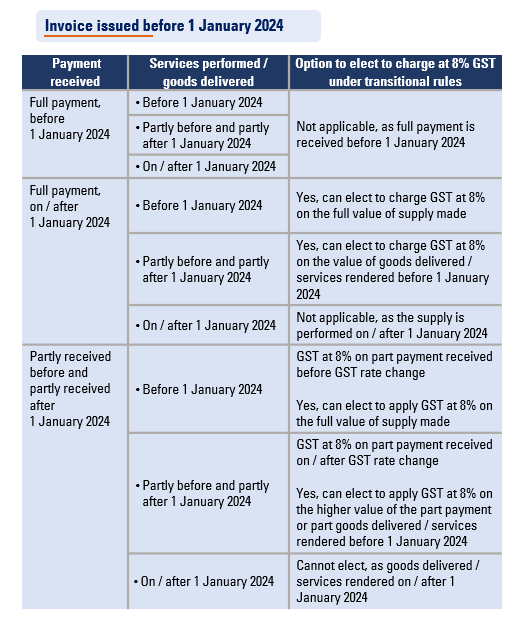

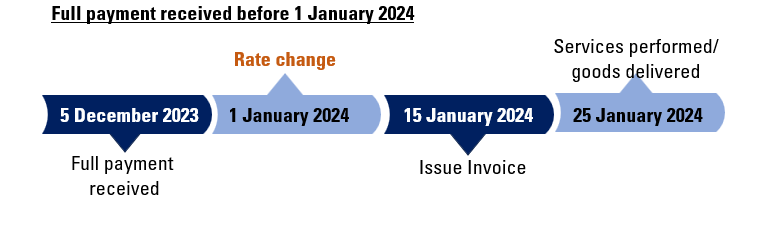

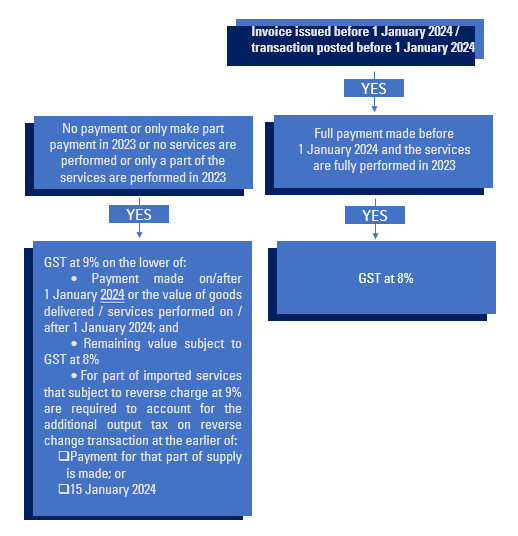

Invoice issued before 1 January 2024

Scenario 1

- Full payment received, or supply completed before rate change / 1 January 2024:

For invoices issued in 2023 and (i) receive full payment in 2023; or (ii) deliver all the goods or perform all the services in 2023, the full value of supply is subject to GST at 8% and no adjustment is required.

Scenario 2

Businesses need to charge and account for GST at 8% on tax invoice issued to customer on 5 December 2023.

As businesses do not receive any payment or deliver all the goods or perform all the services before 1 January 2024, under transitional rules, businesses are required to issue a credit note for the original invoice and a new tax invoice to charge GST at 9% on its supply by 15 January 2024.

Scenario 3

Businesses must charge and account for GST at 8% on tax invoice issued to customer on 18 December 2023. As businesses do not perform any services and only receive part payment before 1 January 2024, under transitional rules, businesses are required to issue credit note and new tax invoice to customer by 15 January 2024, for the part payment received# after 1 January 2024:

• Credit note for SGD756 (SGD700 plus 8% GST of SGD56); and

• A new tax invoice for SGD763 (SGD700 plus 9% GST of SGD63)

# Part payment received after 1 January 2024 (SGD700) is subject to GST at 9% as it is lower than the value of the services performed after 1 January 2024 (SGD1,000).

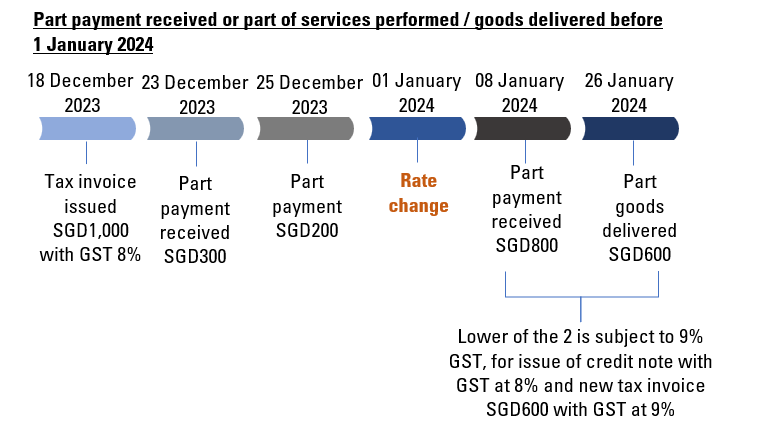

Scenario 4

Businesses must charge and account for GST at 8% on tax invoice issued to customer on 18 December 2023. As businesses only receive part payment and deliver part of goods before 1 January 2024, under transitional rules, businesses are required to issue credit note and new tax invoice to their customer by

15 January 2024, for that part of the goods delivered # after 1 January 2024:

• Credit note for SGD648 (SGD600 plus 8% GST of SGD48); and

• A new tax invoice for SGD654 (SGD600 plus 9% GST of SGD54)

# The value of part goods delivered after 1 January 2024 (SGD600) is subject to GST at 9% as it is lower than the value of part payment received after 1 January 2024 (SGD800).

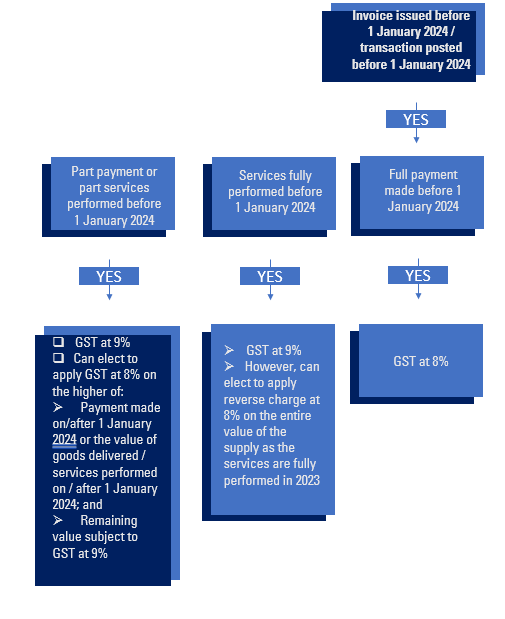

Invoice issued before 1 January 2024

Scenario 1

Scenario 2

For invoices issued on / after 1 January 2024 and full payment occurred before 1 January 2024, the full value of supply is subject GST at 8%. Under transitional rules on 15 January 2024, businesses are required to charge and account for GST at 9%.

However, the supplier can elect to charge GST at 8% on the entire value of the supply as the services fully performed or goods are fully delivered before 1 January 2024.

Scenario 3

For scenario above, as general rule – GST will be chargeable on the supply as follows:

• 8% GST on part payment received before 1 January 2024; and

• 9% GST on part payment received on/after 1 January 2024

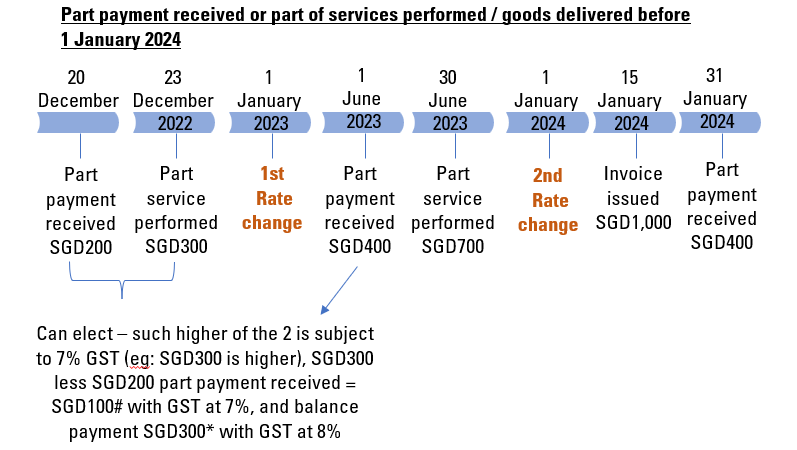

Scenario 4

Scenario 4 cont’d

As general rule, businesses must charge and account for GST at 7% on the part payment of SGD200 received on 20 December 2022 and must also charge and account for GST at 8% on the part payment of SGD400 received on 1 June 2023.

However, under transitional rules, businesses can elect to charge GST at 7% on the higher of :

•Payment received before 1 January 2024 (SGD200); or

•The value of goods delivered, or services performed before 1 January 2023 (SGD300).

Hence, for payment received (SGD400) on 1 June 2023, businesses may elect to account GST at 7% on SGD100# and 8% on SGD300*.

On 15 January 2024, when the invoice is issued, businesses are required to charge and account for GST at 9% on the remaining value of the supply of SGD400

(i.e. SGD1,000 less the value supply on which GST already accounted for previously (SGD200+SGD400=SGD600)).

However, businesses may elect for GST at 8% on the entire SGD400 as the services are fully performed before 1 January 2024.

Continuous supplies of goods and services

Scenario 1

Scenario 2

As general rule, businesses must charge and account for GST at 8% on the tax invoice issued to their customer on 8 December 2023. As you only received part payment and perform part of the maintenance services before 1 January 2024, under transitional rules, businesses are required to issue credit note and new tax invoice to their customer by 15 January 2024, for that part of the payment received after 1 January 2024:

• Credit note for SGD432 (SGD400 plus 8% GST of SGD32); and

• A new tax invoice for SGD436 (SGD400 plus 9% GST of SGD36)

Goods put private use without consideration

Based on general rule, 31 January 2024 is the last day of the prescribed accounting period in which goods are taken for private use. Hence, output tax should be accounted at 9%.

Under the transitional rules, businesses can elect to account for output tax at 8% since all the goods are taken for private use on 20 December 2023 and before 1 January 2024.

Reverse Change Supplies

Reverse Change Supplies

Receipt of Payment

Recurring payments made via Giro deductions and credit card

All payment received through recurring Giro deduction and credit card payment within the month of January 2024 can be treated before 1 January 2024 if following conditions are met:

(a) The Giro deduction or credit card payment is successfully effected by the end of January 2024;

(b) The Giro deduction or credit card payment relates to bills or invoices that are issued before 1 January 2024; and

(c) The bills or invoices in (b) are issued according to the normal billing cycle of the business

Electronic Payment Modes

Following payments can be treated as received before 1 January 2024 even though the actual monies may be received by the supplier on/after 1 January 2024:

- Non-recurring payment charged to the credit card by 31 December 2023;

- Telegraphic transfer (TT) instruction received by the recipient bank by 31 December 2023;

- AXS, SAM or NETS transaction which takes place by 31 December 2023; and

Deductions from a customer’s e-wallet by 31 December 2023

Cash

Payment is treated as received on the date you receive the cash from your customer.

Cheque

Cheques issued to you in 2023 (eg: cheque dated in 2023), and presented to the bank (i.e., the bank-in date) by 4 January 2024 and cleared successfully can be treated as payments received before 1 January 2024.